Why the ‘Rapid Substitution’ of fossil fuels for renewables will crash oil and save consumers money

Cathie Wood made news recently with her prediction that electric vehicles would prevent crude from breaking out, saying she would be “surprised” if oil prices hit $70 again. However, we believe the Ark Capital CEO is only half right: not only are we reaching peak oil prices but expect those prices to collapse as a gradual—yet permanent—move away from petroleum products slides prices down a near-asymptotic supply curve.

Supply

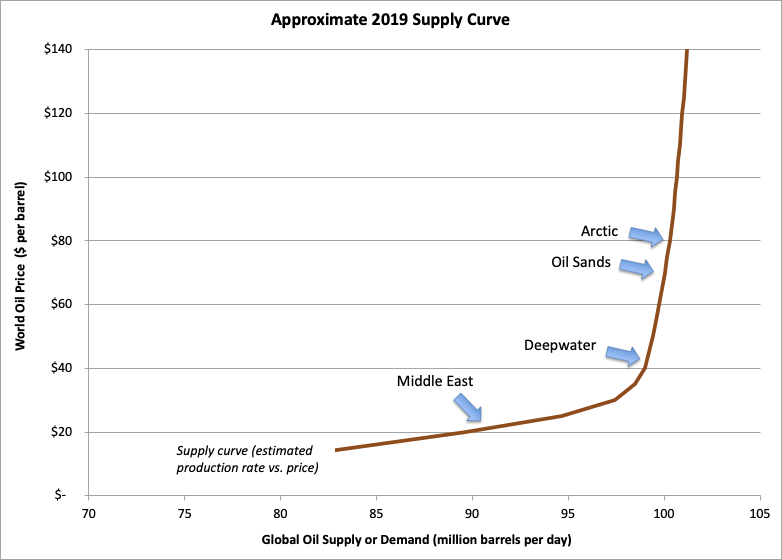

To understand why, it’s important to grasp oil’s supply curve. Consider that the amount of oil that can be produced at any given time is relatively fixed—there is a certain amount of oil that can be easily extracted from the ground and, thus, in the short-term, large increases in demand have a relatively muted effect on the quantity of supply. (Thus, increased demand succeeds merely in driving up price, as desperate consumers compete for the last, marginal barrels of oil).

The nature of oil production makes the supply curve appear like a hockey stick: there is a ‘handle’ portion of the graph, where a gradual increase in price is met by a gradual increase in production (and defined by the world’s more easily extracted oil), followed by a ‘blade’ portion, where the curve turns sharply upwards, demonstrating the increasing difficulty and expense of pumping more oil from the ground. In the blade portion, producers require higher prices in order to undertake the much more costly exploration and production of oil—examples include tar sands, deep water, and arctic drilling. At some point, supply hits a wall where no amount of price increase will result in further, near-term production capacity.

Source: EIA, Rystad Energy, Skibo Energy Analysis

The fact that tar sands and other, unconventional methods of oil extraction have become an increasing portion of global production since 2000 (when prices shifted skywards) tells us something about both the exigent nature of oil demand and the increasing difficulty and expense of oil production.

Enter EVs

But oil demand took a serious hit in 2020, setting up what we believe will be a more permanent shift in the dynamics of oil supply and demand. As renewables begin to replace fossil fuels at a faster clip in a process we call ‘Rapid Substitution,’ demand for petroleum products will buckle, plummeting oil prices back down the gravity well.

Let’s consider EV sales as an example.

In 2020, global sales of electric vehicles (BEV + PHEV) rose by 43% to more than 3 million units (representing 4.2% of the total car market and despite an overall 20% decline in car sales generally). Most of that growth was seen in Europe and China, but as the U.S. market begins a more calculated pivot towards electrification, led by government regulations, legacy automakers, and new EV manufacturers (e.g., Tesla, Rivian), one can expect sales to climb at increasing speeds. A relatively conservative forecast by Deloitte (mid-2020) has US EV sales rising to 27% of market share by 2030. Considering that US transportation accounts for roughly 13.5% of global oil consumption (60% of which is personal vehicles), Deloitte’s forecast equates to a greater than 3% drop in global oil demand by 2030 caused by US EV sales alone.

That number doesn’t account for the possibility of an even more energetic transition fueled by a Biden presidency (the study was done prior to the 2020 election). Catalysts for faster substitution could include Biden’s call for an all-electric Federal fleet, his infrastructure bill, which includes funding for 500,000 EV chargers, or the Clean Transit bill recently introduced by Senators Shumer and Brown. Other policies that would expedite Rapid Substitution include renewable fuel mandates, efficiency standards, the elimination of inefficient fossil fuel subsidies, direct emissions reduction regulations, and continuing federal and state incentive programs for EV consumers and producers.

Combine US EV sales with the much faster adopting Chinese and European markets, and the transition more broadly to renewable energy sources, and you begin to get a picture of the headwinds confronting oil demand. But focusing on EVs alone, and assuming even just a modest substitution, what would a 3% demand drop mean for oil prices?

Oil Demand Pressures – A linear drop in demand results in a geometric drop in price

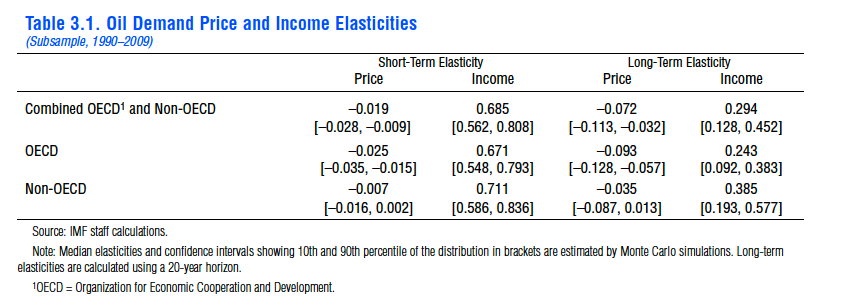

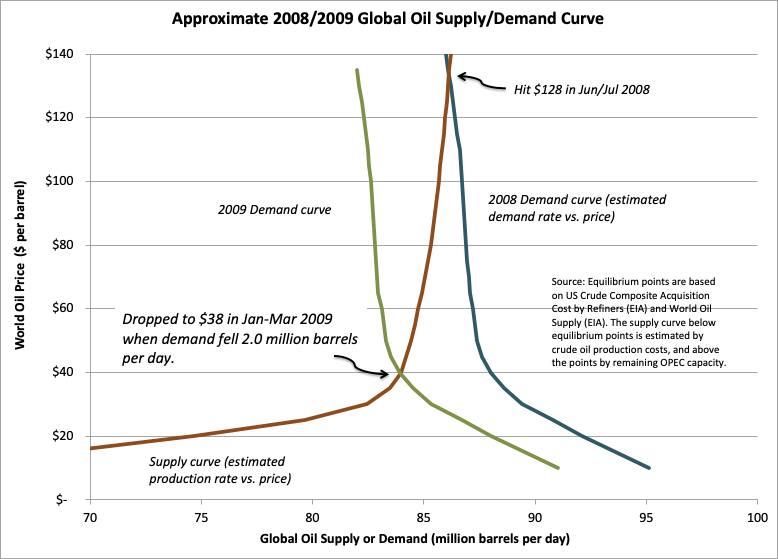

One metric for understanding the effect of a drop in demand on price is the ‘demand price elasticity’. An IMF research paper considering twenty years of historical data suggested that the short-term elasticity of oil demand is –0.019, meaning that the first one percent decline in demand should result in a ~53% price drop. While that number may seem shocking at first glance, consider the oil shock in 2008 when, during a six-month period, a 3% drop in demand was accompanied by a 70% drop in price. Recall that this function can be explained by the shape of the supply curve, where the steepness of the ‘blade’ portion results in exaggerated movements in price in response to changing demand.

Source: IMF

Source: EIA, Skibo Energy Analysis

All things considered, if a similar, albeit more gradual, drop in oil demand results in a likewise disproportionate price drop (utilizing the Long-Term Elasticity figure), we would expect oil prices below $30 by 2030.

But won’t producers respond by curtailing supply to support higher prices?

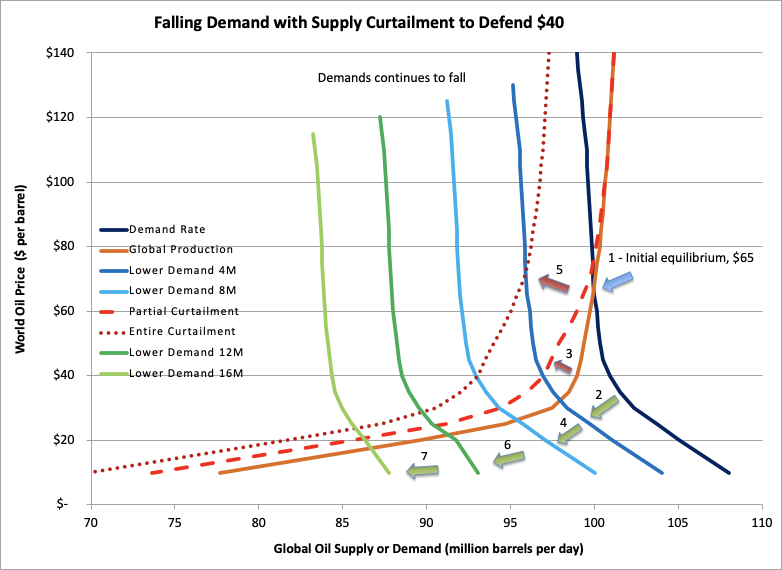

In the short-term, organized efforts by suppliers to curtail production can effectively rebound prices, as happened in 2009 and again when the price of oil crashed in 2020. But curtailment is only a rational strategy for addressing shocks with relatively short, expected time horizons, such as during an economic crash or a pandemic. That same strategy becomes self-destructive in the face of a prolonged, continuous, and systematic decline in demand, as a revolution in vehicle propulsion represents. In this way, the transition to EVs is more analogous to the implementation of auto efficiency standards in the late 1970s, which drove oil demand (and prices) down for the next decade as more fuel-efficient cars gradually replaced their gas-guzzling predecessors. Once suppliers realize that future revenues can only go in one direction, the rational strategy will be to pump while prices remain relatively high, further diluting their premiums. (the ‘get while the gettin’s good’ strategy) This makes sense especially since the lion’s share of production costs are up-front capital costs, while the costs of continued operation are marginal. An oil rig, once operational, can continue pumping for decades at marginal cost to the owner, meaning that even without additional supply coming online, existing supply may support lower prices for years to come.

Source: EIA, Skibo Energy Analysis

In the graph above, the initial equilibrium price of $65 (1) is disrupted by a drop in demand by 4 million barrels per day (2). OPEC and other oil producers respond first with a partial curtailment (3), and then, following another 4MBD demand drop (4), with a more expansive curtailment (5) to defend price at $40 per barrel. Demand continues to fall as ICE vehicles are replaced by EVs (6, 7) to some point (5) where, eventually producers are forced to give-up on their strategy of curtailment. Price continues to fall below $30. Notice, in this example, that a roughly 15% drop in demand results in >50% drop in price.

Broader Significance – Rapid Substitution pays social dividends

The implications of Rapid Substitution’s effect on oil prices are wide-ranging. While many are familiar with the catastrophic futures an energy revolution helps to foreclose (e.g. climate change, pollution, and continued oil exploration in some of the world’s most sensitive ecosystems), few recognize the savings that Rapid Substitution generates for consumers in the form of lower energy costs. While today, most oil is sold well above its cost of production (remember, price is set by the most marginal production required to meet demand and generates tremendous profits for its owners), in the future those profits will be displaced, instead manifesting as lower oil costs for all. Skibo Energy estimates that over the lifetime of an electric vehicle, the amount of oil demand it displaces will represent a more than $100,000 savings to oil consumers generally, a position we will explore in depth in an upcoming blog post. If true, that would mean that the social value of every EV on the road is far greater than is typically understood.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}